When Cheron Robinson, 46, and his wife, Lanette, 48, started looking for a new home in the Atlanta metro area in 2019, they got outbid on the first two homes they were interested in by cash investors. The Robinsons were already homeowners, but to make a cash offer of their own, they would have had to sell their home and rent an apartment while house hunting and closing on a new place.

The Robinsons’ loan officer and agent recommended they try a program called Ribbon, which would allow them to make a cash offer and pay back the loan after they closed on the new place and sold their old home.

“I was skeptical and I didn’t believe it. It sounded too good to be true. It sounded crazy,” Robinson said.

An investor still managed to over-bid them. But after those negotiations fell apart, the Robinsons were next in line and closed the deal. The seller said the house had 60 offers.

“With the Ribbon program, we actually were kicked up” the line “to be able to get placed in there,” he said.

In today’s wildly competitive housing market, typical homebuyers are being beat out by investors and transplants bidding above asking price – with cash. Now, ordinary buyers are turning to services like Ribbon, Flyhomes, Orchard, Accept.inc and Homeward to get a cash advantage.

“We love them,” said Tria Kreutzer, the CEO of the Joe Carbone Team, a Compass affiliate in the Atlanta metro area. Kreutzer uses both Ribbon and Homeward.

“I mean, we pretty much at this point can’t do without them in order to win offers,” she said.

Proponents of cash-offer services say they’re giving regular buyers a shot in today’s market. But critics say some services are too good to be true – they can have unexpected costs, can exacerbate price hikes for the rest of the neighborhood and might be extending the life of this crazy housing cycle. Plus, as interest rates rise, they might become less attractive as higher mortgage payments prevent buyers from paying fees and other costs.

The Robinsons’ quest for a cash bid on their home in Jonesboro is indicative of a larger trend – the increasing pressure on ordinary buyers to find ways to offer cash.

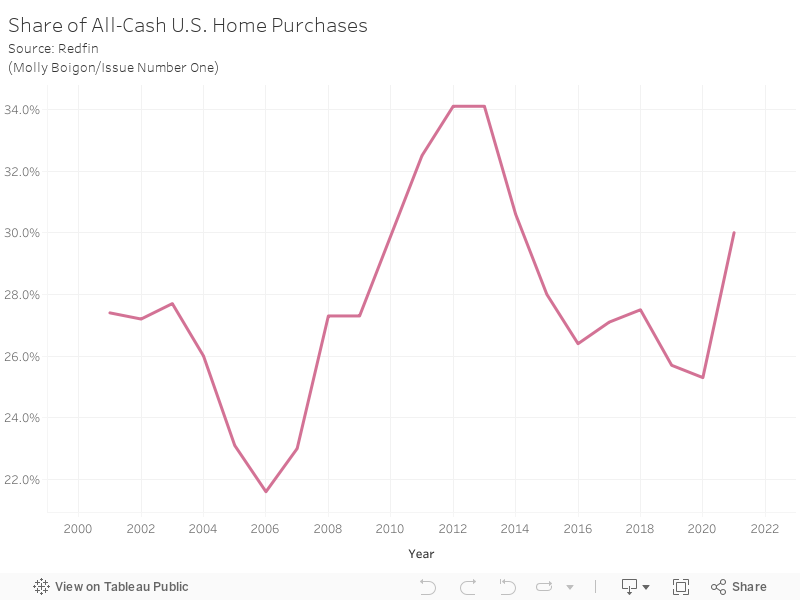

The share of cash offers as part of the larger market has been up and down over the years, according to data from Redfin. But 2021 saw 30 percent of U.S. home purchases paid for with cash, the highest share since 2014.

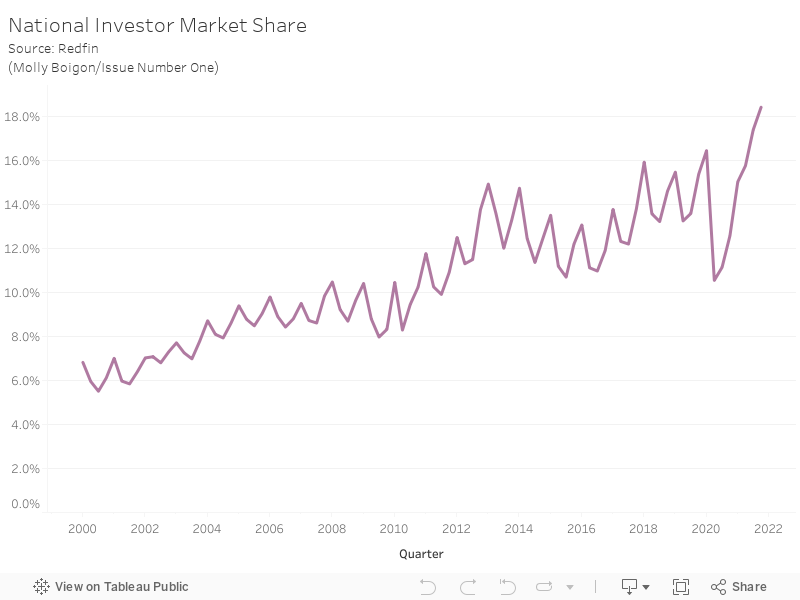

Investors, who made up the largest-ever share of home purchases at the end of 2021 – 18.4 percent – are typically able to pay in cash. And Americans moving from higher-cost markets like New York to lower-cost ones like Atlanta have access to liquid cash from prior sales. That means ordinary buyers may have to pay cash to compete.

The housing market has been running hot from a combination of high demand as a result of Millennials aging out of rentals and their parents’ homes, remote work enabled by the pandemic, low interest rates instituted by the Fed and more than a decade of underbuilding following the 2008 housing crash. Housing inventory only just rebounded to about a six-month supply after it sunk to a 3.5-month supply in August, September and October of 2021.

Sellers are able to pick and choose between a buffet of not only bids financed with more typical loans, but multiple cash offers. For sellers, cash offers are attractive because they are seen as more flexible than offers financed with conventional mortgages or more typical loans. The buyer makes an offer based on the amount of cash in hand, and doesn’t have to abide by the strict requirements of the lender. That makes a cash offer look like more of a sure bet than an offer with other types of financing.

Ribbon and other cash-offer services offer many of the same advantages as normal cash offers.

For some buyers, like those who are moving from one home to another and who don’t have liquidity to make an offer, cash-offer services work as almost a rich uncle that can step in to close on the home if the buyer can’t drum up the cash in time.

Orchard “helps average American families who would otherwise not have the ability to make a cash offer stand out in a hyper-competitive market where cash offers are 4x as likely to get accepted,” Mandy Menaker, a spokesperson for Orchard, said in an email. None of the other services responded to requests for comment.

The process for each service varies. But generally, buyers provide financial information and pre-approval for a loan that qualifies them. The cash-offer service steps in on the buyer’s behalf to make a cash offer.

For first-time homebuyers, the buyer is eventually approved for a more typical loan, like a mortgage, and can use the loan or to pay back the cash-offer service.

For people selling homes, the cash-offer service basically serves as a bridge loan. When the buyer sells a previous home, they can use the money from the last sale to pay back the cash-offer service.

But cash offers have their costs – for loan recipients and for the market.

The approvals process can be opaque. Orchard, for example, publishes neither the terms under which it accepts home buyers for the program nor its acceptance rates. The “bridge loans” offered by these services are not are not subject to the Truth In Lending Act, which requires disclosure of information like how loan payments might rise under different interest-rate scenarios and bans loan officers from pushing loans that might not be in the consumer’s best interest.

There can also be unexpected costs. The Robinsons agreed to pay a certain amount of “rent” to Ribbon while they waited to get the loan from the V.A. to repay the cash. The appraisal took months longer than expected because the V.A. office was not familiar with cash-offer services. The Robinsons ended up paying more than $2,000 a month to Ribbon from July through October until they finally bought the house back.

“The deal kind of got a little crazy,” Robinson said. “It didn’t go as sweet as we planned it.”

Cash-offer services often agree to a maximum offer amount before the appraisal and will cover the gap if the appraisal comes in lower than the offer. When buyers using cash-offer services – or more typical cash buyers – are able to close above the appraisal, that hikes prices across the whole neighborhood. That may not happen for every sale, but sellers look at comparable homes that closed recently, sometimes called “comps,” to determine listing price.

“It then drives the price up of that community, regardless if the value is there or not, because the property has been purchased cash, which still becomes a viable comp,” said Penny Williams, an associate broker with Better Homes and Gardens Metro Brokers in the Atlanta metro area and the Robinsons’ agent.

On a macro level, it’s possible that cash-offer services are artificially extending the boom of the housing cycle. Buyers can navigate around mortgages – even as interest rates increase – as in the case of people selling homes and then using cash-offer services to buy before the money comes through. That, in combination with cash purchases from investors and transplants, extends demand.

“You’re extending the life of the housing cycle and facilitating greater upward pressure on price,” said Domonic Purviance, a subject matter expert in real estate at the Federal Reserve Bank of Atlanta.

The Fed is raising short-term interest rates in part to slow demand and shrink prices. Whitney Hanna, the team lead of the Hanna Legacy Group with Norman and Associates in Atlanta, said she suspects that cash-offer services might get less popular because the thought of making higher mortgage payments, paying fees and possibly forking over rent is not attractive.

“Everybody’s looking at their expenses like” cash-offer services are “a good idea, but can we afford it?” she said. “Do I really want to buy a house and be house poor when I move in?”